What is the VAT for travel agencies?

Value Added Tax (VAT) is an indirect tax applied to consumption.

In tourism, it takes a particular form, as travel agencies sell complex services combining transport, accommodation, tours, or insurance. These services are often purchased and resold by intermediaries located in different countries, making VAT more difficult to apply than simple local commerce.

Unlike traditional merchants, agencies do not charge VAT on each component of the trip. They are subject to a specific regime called the “margin scheme,” established to avoid double taxation of services included in a package tour.

This specificity is based on two pillars:

- A European directive (2006/112/EC) that harmonizes the treatment of VAT in tourism to facilitate fair competition among European operators.

- A taxation on the margin: only the difference between the selling price of the trip and the cost of purchasing the services is subject to VAT.

This regime applies when the tour operator acts in its own name and sells a product combining at least two services (e.g.: transport + accommodation). It establishes a simplified but rigorously regulated system, especially for sales made within the European Union.

To better understand how VAT fits into the overall logic of a travel agency, also check out our article on managing tourist reservations.

How to distinguish the different VAT regimes applicable to a travel agency?

Identifying the correct VAT regime is a strategic issue for any agency. Between public package tours, B2B contracts, or corporate stays, the boundary is not always clear. Here are the main regimes to know to remain compliant.

The margin scheme (Article 306 of the General Tax Code)

It applies to agencies that sell stays or services in their own name, without detailing the services separately. VAT is then calculated only on the profit margin, and not on the total cost.

- Applicable to sales to individual travelers.

- Not deductible on purchases related to these sales (accommodation, transport, etc.).

- VAT due upon receipt of the total price of the trip.

The common law regime

If the agency acts as a simple intermediary — for example, by charging commissions — it falls under the traditional VAT regime. It charges tax only on its fees and can deduct VAT on the corresponding purchases.

- Applicable to agencies operating on behalf of another tourism professional.

- Often used in the context of subcontracting or the sale of individual tickets.

Particular cases: business trips, subcontracting, and B2B

Business or incentive trips ordered by companies follow specific rules. The treatment depends on the place of consumption of the service and the type of client. For example:

- Services outside the European Union may be exempt from VAT.

- A subcontracting contract between two tourism professionals may fall under common law.

To deepen these distinctions and anticipate the impacts on your B2B strategy, consult our guide on GetYourGuide and Viator, two platforms that often change the applicable VAT regime depending on the role played by the agency.

Specifically, what VAT rate for a travel agency?

It will depend on the products resold by the agency. Here’s the overview.

1. Particular regime for travel agencies (Article 306 of the VAT directive / Article 266 of the CGI in France)

When an agency sells “all-inclusive” trips (transport, accommodation, excursions…) for its own account, it is subject to a special VAT regime:

- VAT is calculated only on the agency’s margin (and not on the total price charged to the client).

- The VAT rate applied to this margin is the normal rate:

👉 20% in metropolitan France.

🧮 Example:

A client pays €1,000 for a trip. The agency pays €800 to the providers (hotel, transport). Its margin = €200. VAT = 20% on €200 = €40.

2. Agency acting as an intermediary (mandatary)

If the agency acts on behalf of the client (for example, it sells a plane ticket for an airline and receives a commission), then:

- The agency’s service (its commission) is subject to VAT at the normal rate of 20%.

- The international transport of passengers itself may be exempt from VAT (Article 262 of the CGI).

3. Trips outside the European Union

For trips where the services are provided outside the EU, the corresponding part of the trip is exempt from VAT.

👉 Only the part of the trip carried out in the EU remains subject to VAT (20% on the corresponding margin).

How to calculate and declare VAT on the margin in a travel agency?

Calculating VAT on the margin is not a complex operation, but it requires a rigorous method. Every euro misallocated can have a direct impact on your net result and tax compliance. Here’s the procedure to follow to properly apply this regime.

Steps for calculating the taxable margin

The first step is to precisely define the taxable base. The margin corresponds to the difference between:

- The total price paid by the client (including tax);

- And the cost of purchasing the services from third-party suppliers (transporters, hotels, tour guides, etc.).

In other words: margin = selling price – cost of purchasing the provided services.

This margin, and only this margin, is subject to VAT.

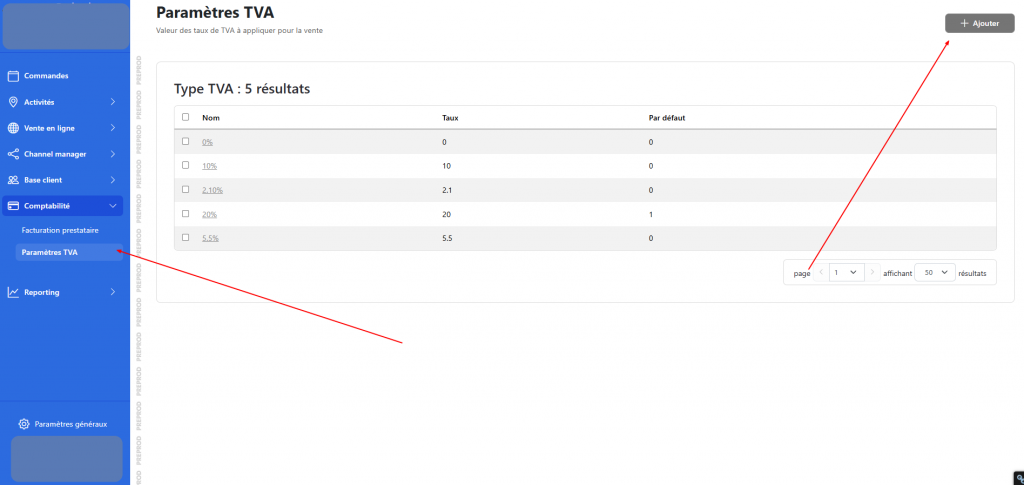

Determination of the applicable rate

The rate depends on the location of the service:

- Trips in France: normal rate of 20% on the margin.

- Trips in the European Union: subject to the French rate if the agency is established in France.

- Trips carried out outside the EU: exemption from VAT on the corresponding margin.

A correct allocation of operations is therefore essential, especially if your packages combine several destinations.

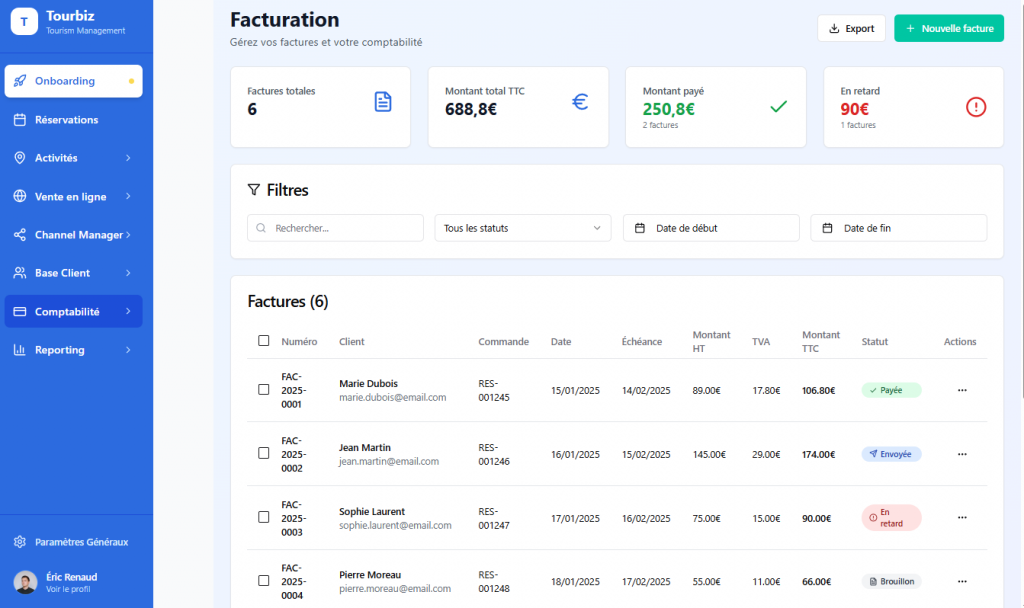

Declaration and payment of VAT

Agencies must declare the VAT collected on the margin at each period (monthly or quarterly depending on the regime).

The amounts are to be reported on the CA3 declaration, generally in the box dedicated to operations subject to VAT on the margin.

Some essential tips:

- Keep a clear record of purchase costs and sales.

- Keep supplier invoices for each operation.

- Avoid mixing services subject to the margin and services under common law.

For better accuracy in your calculations, discover how to optimize your sales and prices in our article on dynamic pricing.

What tools to use to simplify VAT management as a travel agency?

Good news: managing VAT on the margin no longer necessarily means administrative headaches.

The right tools can automate your calculations, centralize your invoices, and secure your tax declarations.

Compatible invoicing software

Choose a solution that specifically manages the margin scheme. These software allow:

- To automatically isolate the components subject to VAT and those that are not;

- To calculate the taxable margin on each client file;

- To generate invoices compliant with regulations.

Accounting tracking and tax compliance tools

SaaS platforms specialized in tourism, like Tourbiz, centralize your accounting flows: supplier invoices, receipts, client payments.

They simplify the preparation of declarations thanks to exports compatible with your accountant.

Good automation practices

To limit errors and save time:

- Automate the entry of supplier invoices;

- Synchronize your sales from your partner platforms;

- Schedule alerts for tax deadlines.

Finally, consider interconnecting your tools through a channel manager. It facilitates multi-platform management (OTAs, partners, local agencies) and automatically synchronizes your sales data, your margins, and the associated VAT rates.

How does Tourbiz facilitate VAT management and declaration for travel agencies?

Managing VAT in tourism often means navigating between several regimes, rates, and countries. With its integrations and intelligent accounting engine, Tourbiz transforms this complexity into a smooth and automated process. Designed for travel professionals, the software adapts to the reality of your activity – whether it involves B2C sales, contracts with OTAs, or tailor-made packages.

Automatic integration of accounting and invoicing data

Tourbiz connects your data sources (booking platforms, CRM, suppliers, payments) to centralize all your accounting. Each invoice, each receipt is analyzed and allocated according to the correct VAT regime.

- Automatic update of VAT collected on the margin;

- Direct import of supplier invoices and association with corresponding sales;

- Accounting exports compliant with the required format for the CA3 declaration.

Result : no more double entries, fewer errors, and an instant view of your total amounts including tax vs. excluding tax.

Configuration of the VAT regime according to activity and destination

Each agency has its specificities : tours in France, in Europe, cruises, or stays outside the EU. Tourbiz allows you to precisely configure the applicable regime for each type of activity.

- Choice of regime (margin or common law) at the creation of the client file;

- Automatic allocation of rates according to destinations;

- Preview of the VAT amount before validating the quote.

This intelligent configuration ensures that your margins, your rates, and your invoices are aligned with current regulations — without wasting time or accounting approximations.

Seamless synchronization with your online partners

Tourbiz also stands out for its ability to connect with major platforms in the sector.

For example, during a sale made via GetYourGuide, the software automatically retrieves the amounts collected, the OTA commission, and the country of consumption of the service.

- The VAT on the margin is recalculated according to the geographical area;

- Accounting entries are generated in real-time;

- Sales reports include the VAT due at each deadline.

This native synchronization avoids discrepancies between platforms and internal accounting, a real asset for agencies multiplying sales sources and international partners.

In summary, Tourbiz makes VAT a mastered subject, more than an administrative headache. You maintain control, without neglecting your compliance. And above all, you save time for what really matters : your business development and the satisfaction of your travelers.